- cross-posted to:

- amd

- cross-posted to:

- amd

You must log in or # to comment.

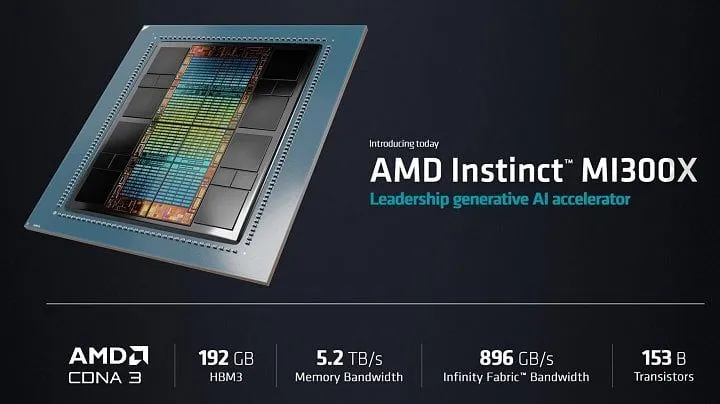

“We now expect datacenter GPU revenue to be approximately $400 million in the fourth quarter and exceed $2 billion in 2024 as revenue ramps throughout the year,” said Lisa Su, chief executive of AMD, at the company’s earnings call with analysts and investors. “This growth would make MI300 the fastest product to ramp to $1 billion in sales in AMD history.”

About what portion of this datacentre GPU revenue is service/support related as opposed to just furnishing the hardware?

Can someone explain to me how this is different from Nvidia offerings? Is it just price difference if the supported software are mostly similar?

As far as software is concerned, AMD has broadened its AI software ecosystem, achieving significant advancements in enhancing the performance and features of its ROCm platform this past quarter. Besides, ROCm has been integrated into the mainstream PyTorch and TensorFlow ecosystems. Furthermore, Hugging Face models are now consistently updated and validated to run on AMD hardware in general and Instinct accelerators in particular.

Kind of wonder RDNA4 won’t just be on 4nm, just to keep all of 3nm for data center chips like this.

The chips is amazing and amd eco system is working " barely well" enough for business to find it worth it to take the plunge.